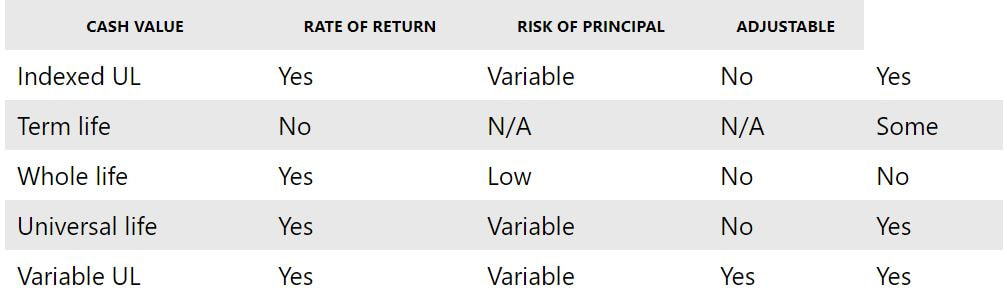

In a nutshell, an indexed universal life insurance policy (IUL) is a form of universal life insurance that pays interest based on the performance of a financial index chosen by your insurer, such as the S&P 500 stock market. The term of this type of policy is divided into crediting periods, also called index periods, which typically range from one month to two years. When the index rises during a given crediting period, the insurance company will credit your policy's cash value with a corresponding amount of interest rather than a fixed interest rate. Indexed universal life insurance policies also normally provide an interest rate guarantee. Those who use the longest crediting periods usually earn the most interest. In most cases, the amount of interest that you can earn during a given crediting period is limited, just like it is with indexed annuities. These limits come in three forms: A "cap" – This is an absolute limit on the amount of interest that is paid. For example, if the benchmark index rises by 30% during a given crediting period, then you may only be able to receive 10% of the growth. The insurance company will keep the difference. A "spread" – This is an amount that the insurance company takes off the top during every crediting period. If the index rises by five percent during a crediting period and your policy has a spread of two percent, then the insurer keeps the first two percent and lets you take the remaining three percent. A "par" rate – This is a participation rate that is a percentage of the growth of the index. If your policy has an 80% par rate, then you will be credited with interest equal to 80% of the growth of the index during that crediting period. Indexed universal life insurance has the same premium and death benefit flexibilities that are found in standard universal life policies. Monthly premiums are adjustable and generally decrease over time as your cash value account increases. Death benefits are also flexible and often have the ability to be lowered or raised at any time. Though your IUL cash value can be accessed freely, it is recommended that this is done with caution as doing so could result in reducing your death benefit or lapsing your account. Who needs indexed universal life insurance? Anyone who is looking for a long-term or permanent life insurance policy, which has the potential to grow cash value at a faster rate than other whole or universal life policies, is a prime candidate for an IUL. Policyholders earn interest at a variable rate and can earn a higher average rate of return over time without risking their money in the stock markets. Indexed universal life insurance vs. other types of life insurance The following table illustrates the similarities and differences between indexed universal life insurance compared with other types of life insurance policies:  Indexed universal life insurance resembles traditional universal life insurance more than any other type of policy. The main difference involves how interest in the cash value is generated. IULs generally have an edge over regular ULs when it comes to overall rate of return, at about 1.5-2% more on average.

Pros and cons of indexed universal life insurance Pros Cash value accumulation Indexed universal life insurance policies have a cash value component which is the part of the policy that is available to you for use while you're still alive. You can use it for anything you want from sending your kids to college to taking a vacation. However, be careful because if you don't pay it all back it can impact the death benefit left to your loved ones. If you don't deplete your cash value by withdrawing from it then this amount (in addition to your death benefit) will be left to your beneficiaries when you die. Tax-free withdrawals The best part about taking money from your cash value? You don't have to pay taxes on it. This is because you've already paid income tax on the money before you've contributed it to your life insurance policy – so you won't have to pay taxes on it again. Adjustable premiums and death benefits Your premiums will adjust over the life of your policy based on the amount of money that's in your cash value component. This allows you to save some money in the long run. Cons Expense Indexed universal life insurance is expensive – in fact, it's one of the most expensive life insurance types out there. It's definitely more expensive than a term policy and so it may be worth considering a more affordable investment option. Variable Interest Rates Your interest rates will vary based on how your money is invested. As the indexes go up, the interest you earn will rise. However, that means that the interest you're earning can go down – or disappear altogether. You're at the mercy of the stock market with this kind of policy. Source: money.msn.com

0 Comments

A life insurance retirement plan (LIRP) can be an effective complement to traditional forms of retirement savings like IRAs or company-sponsored retirement plans. This type of plan does not have many of the distribution-related restrictions that IRAs and qualified plans are saddled with. Although an LIRP is not designed to replace traditional avenues of saving for retirement, it can provide substantial benefits under the right circumstances. Life Insurance Retirement Plans Explained A life insurance retirement plan is a permanent, or cash value life insurance policy that is funded over time, in order to build up a substantial amount of cash value by the time you retire. You can use any type of cash value policy to do this, but some types of coverage have historically grown faster than others - although the policyholder might have had to take on some market risk to get there. LIRPs are designed to provide retirement savers with a supplemental source of income on top of their IRA and retirement plan distributions, after they stop working. LIRPs do not offer some of the tax advantages that IRAs and qualified plans can provide, such as pre-tax or deductible contributions. But they can also provide a few benefits that IRAs and qualified plans cannot match. For example, there is no age requirement for distributions (in the form of tax-free loans) from a LIRP. IRAs and qualified plans will penalize you for any distributions taken before age 59 1/2 , unless a qualified exception applies. Furthermore, LIRPs can often guarantee the investor's principal and interest, unless the investor is contributing to a variable universal life insurance policy. How to Fund Retirement With a LIRP Funding a life insurance retirement plan is very simple. It just requires taking out a cash value life insurance policy for the amount of coverage that you want, then overfunding it by paying more than the minimum required premiums. The excess amount will go into the cash value of the policy and start building it up faster than it would otherwise. This is one of the simplest forms of retirement saving, as there are very few rules that dictate the process. If you want your policy to grow faster over time, consider investing in a variable universal life policy that invests its cash value in the financial markets. There is more risk with this type of policy, but also more reward. Or you could invest in an indexed universal life policy, where you can make money when the financial indices rise but not lose anything when they fall. It all depends on your risk tolerance and time horizon. When you retire, you can take tax-free distributions from your accumulated cash value in the form of policy loans. Of course, it is also possible to take tax-free distributions from your Roth IRA if you have one, but the Roth doesn't also offer death benefit protection and has limits on how much you can put in it each year. Who Needs a Life Insurance Retirement Plan? In the majority of the time, there are three main situations where a LIRP can be appropriate for retirement savers:

Frequently Asked Questions:

What are the best life insurance policies to use for a LIRP? There is no single "best" policy to use for a LIRP; it all depends upon your risk tolerance, time horizon and the amount of money that you're willing to invest. Universal life and indexed universal life policies pay variable rates of interest, but over time they have usually done better than whole life insurance. Risk-takers will want to take a look at variable universal life policies, where there is no limit on their earnings-or losses. How long have LIRPs been around? LIRPs have existed since the first modern commercial cash value life insurance policies were introduced. Anyone who could afford the premiums could set up a LIRP. Higher-income consumers have been using them ever since. But they have become more prevalent with the advent of universal, indexed and variable universal policies that allow the cash value to grow faster than it can inside a traditional whole life policy. How risky are LIRPs compared to IRAs and other retirement plans? It all depends on what type of policy you buy for your LIRP versus what investments you choose in the other alternatives. If you use a whole, universal or indexed universal life policy, then your principal is guaranteed, although the interest rate is variable with the latter two options. If you invest in a variable universal life policy, then you can earn hefty returns when the market goes up. But, of course, the markets don't always do that. The other factor to consider is what you are investing in inside of your IRA or company-sponsored retirement plan. If you are investing primarily in stocks, then you're taking the same amount of risk that you would take with a variable universal policy. If you are investing in government bonds or CDs, then you're taking about as much risk as you are with a whole life policy. You may be contributing to an IRA or qualified plan and have a specific policy in mind to use as a LIRP. If that is the case, it may be wise for you to consult with your financial advisor to compare them. Source: MSN Money |

Archives

February 2022

Categories |

RSS Feed

RSS Feed

USA Mutual Insurance Agency, LLC | 4830 Arthur Kill Road, LL1 Staten Island, NY 10309 | (718) 285-6500 | [email protected]