A life insurance retirement plan (LIRP) can be an effective complement to traditional forms of retirement savings like IRAs or company-sponsored retirement plans. This type of plan does not have many of the distribution-related restrictions that IRAs and qualified plans are saddled with. Although an LIRP is not designed to replace traditional avenues of saving for retirement, it can provide substantial benefits under the right circumstances. Life Insurance Retirement Plans Explained A life insurance retirement plan is a permanent, or cash value life insurance policy that is funded over time, in order to build up a substantial amount of cash value by the time you retire. You can use any type of cash value policy to do this, but some types of coverage have historically grown faster than others - although the policyholder might have had to take on some market risk to get there. LIRPs are designed to provide retirement savers with a supplemental source of income on top of their IRA and retirement plan distributions, after they stop working. LIRPs do not offer some of the tax advantages that IRAs and qualified plans can provide, such as pre-tax or deductible contributions. But they can also provide a few benefits that IRAs and qualified plans cannot match. For example, there is no age requirement for distributions (in the form of tax-free loans) from a LIRP. IRAs and qualified plans will penalize you for any distributions taken before age 59 1/2 , unless a qualified exception applies. Furthermore, LIRPs can often guarantee the investor's principal and interest, unless the investor is contributing to a variable universal life insurance policy. How to Fund Retirement With a LIRP Funding a life insurance retirement plan is very simple. It just requires taking out a cash value life insurance policy for the amount of coverage that you want, then overfunding it by paying more than the minimum required premiums. The excess amount will go into the cash value of the policy and start building it up faster than it would otherwise. This is one of the simplest forms of retirement saving, as there are very few rules that dictate the process. If you want your policy to grow faster over time, consider investing in a variable universal life policy that invests its cash value in the financial markets. There is more risk with this type of policy, but also more reward. Or you could invest in an indexed universal life policy, where you can make money when the financial indices rise but not lose anything when they fall. It all depends on your risk tolerance and time horizon. When you retire, you can take tax-free distributions from your accumulated cash value in the form of policy loans. Of course, it is also possible to take tax-free distributions from your Roth IRA if you have one, but the Roth doesn't also offer death benefit protection and has limits on how much you can put in it each year. Who Needs a Life Insurance Retirement Plan? In the majority of the time, there are three main situations where a LIRP can be appropriate for retirement savers:

Frequently Asked Questions:

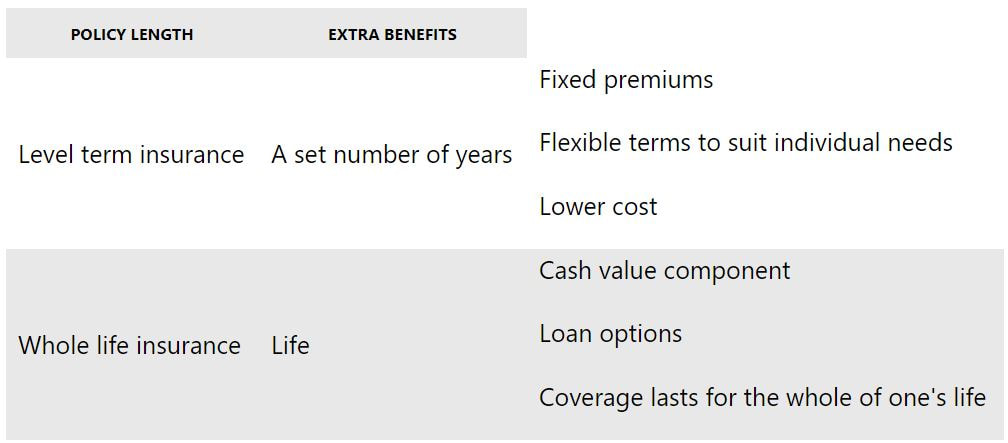

What are the best life insurance policies to use for a LIRP? There is no single "best" policy to use for a LIRP; it all depends upon your risk tolerance, time horizon and the amount of money that you're willing to invest. Universal life and indexed universal life policies pay variable rates of interest, but over time they have usually done better than whole life insurance. Risk-takers will want to take a look at variable universal life policies, where there is no limit on their earnings-or losses. How long have LIRPs been around? LIRPs have existed since the first modern commercial cash value life insurance policies were introduced. Anyone who could afford the premiums could set up a LIRP. Higher-income consumers have been using them ever since. But they have become more prevalent with the advent of universal, indexed and variable universal policies that allow the cash value to grow faster than it can inside a traditional whole life policy. How risky are LIRPs compared to IRAs and other retirement plans? It all depends on what type of policy you buy for your LIRP versus what investments you choose in the other alternatives. If you use a whole, universal or indexed universal life policy, then your principal is guaranteed, although the interest rate is variable with the latter two options. If you invest in a variable universal life policy, then you can earn hefty returns when the market goes up. But, of course, the markets don't always do that. The other factor to consider is what you are investing in inside of your IRA or company-sponsored retirement plan. If you are investing primarily in stocks, then you're taking the same amount of risk that you would take with a variable universal policy. If you are investing in government bonds or CDs, then you're taking about as much risk as you are with a whole life policy. You may be contributing to an IRA or qualified plan and have a specific policy in mind to use as a LIRP. If that is the case, it may be wise for you to consult with your financial advisor to compare them. Source: MSN Money

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Archives

February 2022

Categories |

RSS Feed

RSS Feed

USA Mutual Insurance Agency, LLC | 4830 Arthur Kill Road, LL1 Staten Island, NY 10309 | (718) 285-6500 | [email protected]