The pandemic has fundamentally changed the way Americans shop for essentials. Clothing, groceries and even prescription drugs are increasingly purchased online.

What they’re shopping for has changed as well. Applications for life insurance policies jumped 4% in 2020 — marking the highest year-over-year annual growth rate since 2001. But while you can shop for almost anything else from the comfort of your couch — even other other forms of insurance, like auto, through comparison-shopping sites — until now, the process of buying life insurance has been much more complicated, including going to an in-person doctor’s appointment for a medical exam. Some consumers have been left wondering whether finding an affordable life insurance policy means having to ignore public safety guidelines. But the pandemic has caused a proliferation of the availability of no-exam life insurance, which you can get without leaving your home — meaning you don’t have to choose between protecting your family’s future and your own health. How has the pandemic changed life insurance? No-exam life insurance has been around for a long time. Until recently, it was the only option for high-risk individuals living with medical conditions or working dangerous jobs that make it hard to lock in life insurance. But when the pandemic hit, having to travel to do a medical exam became more than an annoyance — it suddenly wasn’t safe. In response, more than a third of life insurers have now expanded their offerings of accelerated underwriting during the pandemic. With no-exam life insurance, you can skip the medical exam with its blood draws, urine tests and uncomfortable questions. You’ll simply fill out an application, and within minutes you’ll see the option you qualify for — and be able to immediately secure the coverage your family needs. How does the process usually work? Medical exams have long been an important part of the underwriting process for life insurance. Each insurer has its own underwriting process, but generally after you submit an application, you’ll have to do a phone interview with an underwriter, take a medical exam and then allow the insurer to check whether you’ve applied for other life insurance policies and look into your prescription drug and driving history over the last few years. From there, an adviser will go through all the information to come up with a life expectancy and based on that, give you a quote. This whole process can take up to two months. How are some insurers adapting? While insurers are aware consumers want the process to be easier, they also can’t just assign rates without some underwriting. They first need to make sure they’re not overpromising because underdelivering in this situation would mean being unable to pay out claims as they come in — which could be disastrous. And in some states, they also need to be able to legally justify their reasoning for coming up with rates in case an applicant ever contests their offers. So getting rid of underwriting isn’t realistic. But over the last few years, some insurers have been using data and analytics to speed up and streamline the process. At this point, there’s more than enough data out there on most categories of life insurance applicants to accurately calculate a fair premium without having to subject the person to a medical exam. Some brokers can now even show you a quote within minutes of submitting your application. What this means for you Some online insurance companies can now take the information you provide through your application and run it through an algorithm that assesses your risk. If you qualify, you’ll get coverage right away, without ever having to talk to anyone on the phone or taking a medical exam. At a time when it feels like so many choices have been limited for us, you won’t have to choose between security and safety. If you’ve been holding off on buying life insurance because you can’t safely leave your home or you think it’s going to cost an arm and a leg to opt out of a medical exam, you now have options. Source: MSN Money

0 Comments

If you’re going through a divorce, life insurance may be low on your list of priorities, but any policies you purchased during your marriage could be considered marital property and may be subject to distribution. That said, the reason to sort out your life insurance with your former spouse is less to protect your financial interests than those of your children — if you have any.

Divorce proceedings typically differ from state to state. Still, insurance will likely come up during a divorce settlement negotiation, especially if there are children involved and the primary parent earns significantly more than the non-primary parent. Almost anything can be negotiable in a divorce case, and life insurance may be no different. Here’s a quick guide to what to expect if you’re divorcing and one or both of the partners has insurance. Term life insurance simplifies the split Whether or not you’ll have the option of splitting your life insurance with your ex will mainly depend on the type of policy you have: term or permanent. As the name implies, term life insurance covers a temporary financial need with a death benefit that expires between 10 to 30 years. If you, the insured, died within that timespan, your beneficiaries would receive a payout for the face value of the policy. Commonly, policyholders tend to choose a term that expires right around the time their significant expenses are over — after the kids have moved out or their mortgage is paid off. As for the death benefit, the golden rule of thumb is to purchase 10 to 15 times your annual income, although that will depend on your financial needs. Since term life insurance is a simple product that holds no cash value while you’re alive, this type of policy would not be treated as a marital asset during divorce proceedings. If you bought a term life policy while you were with your ex, the policy would likely be considered separate property because the financial asset in the term policy is the death benefit. Whole life insurance can complicate matters Conversely, permanent policies such as whole, indexed, variable, and universal life insurance do not expire as long as the policyholder pays the premiums. And these policies have an investment component known as “cash value” that could be considered a marital asset and may need to be split. Since the life insurance policy itself cannot be split in two, both parties can negotiate the value of that cash component in exchange for another asset. This means that if you wanted to split your shared permanent policy, you’d have to cash it out and divide the proceeds or use the cash payout to cover legal fees or joint debts. And this is typically the most viable course of action for many, as permanent policies are expensive to maintain. Naturally, many divorcées have a change in their monthly cash flow after splitting. Taking the expensive monthly premium of a whole life policy out of the picture can help alleviate costs. Life insurance for the sake of the kids If there are children involved, you may still have a financial obligation to your ex after the divorce settlement — or they to you. In these instances, there may be the need to maintain an existing life insurance policy or take out a new one, in the ex-spouse’s name, to protect alimony payments, child support, and pension or retirement funds. A new policy may be needed if your spouse is in danger of not being able to cover their obligations to the kids were he or she to die. Ideally, the spouse themselves recognizes this vulnerability and is willing and able to take out (and pay for) the policy, or at least agrees to do so as part of a divorce settlement. If that isn’t the case, though, you may want to consider taking out a policy on your ex, to benefit you and your kids. Even if you plan to pay the premiums, however, you will need your ex’s co-operation to buy the policy. Its approval will require their agreement to share personal medical information and perhaps to undergo a medical exam. The process is potentially simpler with an existing policy, especially if you’re prepared to pay the premiums. Keeping a policy on your ex-spouse especially makes sense if they have developed potentially life-threatening medical issues since the policy was taken out. It may also be wise if he or she is in a risky line of work, such as firefighting, policing, or construction. In that case, you could keep a term life policy on them as a precautionary measure. “If your ex runs into burning buildings or operates dangerous equipment for a living. Expect life insurance to be part of divorce negotiations The decision on whether or not to keep a life insurance policy on an ex will be part of the settlement agreement negotiation. If the ex that is paying for the policy is comfortable with maintaining it, the policy can remain. If the ex has no interest in providing coverage, it will be impossible to keep the policy, as it has to be a mutual agreement. Once you get a divorce, you should aim to gain ownership of any policies your former spouse took out on your life because only they can modify the beneficiary designation on the policies. Even if you’re the policyholder, the judge could allow your former spouse to remain as a beneficiary if you owe them child support or alimony. While you can name your children as beneficiaries, it can be complicated if they are minors. Therefore, you could establish a trust with a managing trustee that can help legally divide your death benefit between your children. This can be a good option when you don’t want or can’t trust your ex-spouse with the responsibility. Choosing between term life and another policy type Legal wrangling aside, if you and your ex need to purchase a new policy after your divorce, you’ll need to determine if term or permanent life insurance is the best choice. Term life will cover you for a predetermined period and is a popular option for most people looking for standard coverage, but higher net-worth individuals or people with special needs children could benefit from a permanent policy. Finally, one of the most important things you can do to stabilize your financial future when getting divorced is to plan for the long term. After divorce, before you make any big moves, meet with a financial planner to understand the role life insurance plays in your larger financial picture. This should be a central part of your financial plan, especially if you have kids. Source: MSN Money  Insurance is notoriously complicated, and few people have the time or desire to pore over their policies. But some basic knowledge can go a long way — and that’s where an insurance agent can help, by clearing up some of the most common misconceptions they encounter.

Here are five things agents say are helpful for customers to know. Insurance doesn’t cover everything When it comes to insurance, “Most people don’t understand the details. For instance, they often don’t realize that most homeowners policies won’t cover flood or earthquake damage. If your home is at risk for these disasters, you need separate coverage. Auto policies generally cover only personal use of your car, so if you’ve picked up a side gig delivering groceries or meals during the pandemic, you likely need additional coverage. Otherwise, accidents you have on the job may not be covered. Insurance policies of all types also generally exclude wear and tear. Agents often gets calls from policyholders asking if their insurance will pay for things like broken dishwashers or aging gutters. The answer is no. Insurance is designed to cover sudden, accidental damage, not regular maintenance. A gap in coverage can be costly There are various reasons you might let your car insurance policy lapse, whether you’re having trouble paying your bills or you no longer own a vehicle. But this could cost you. People tend to shop insurance after they’ve already canceled their insurance, [but] unfortunately that’s a huge negative when calculating your price. After a gap in coverage, insurers view customers as riskier and charge higher rates. You can avoid this by shopping for quotes before your policy expires, buying non-owner car insurance if you’re between vehicles and asking your carrier for leniency if you’re struggling to make payments. You can’t get coverage for something that’s already happened. If you get into an accident and your car needs repairs, you might want a rental vehicle to help you get around. But by that point it would be too late to add that coverage, Your auto policy would pay for this only if you had rental car coverage in place when the accident happened — not if you added it the day after. The same goes for other insurance. For example, say a storm leaves an inch of water in your basement, but you haven’t purchased flood insurance. You can still buy coverage for future disasters, but it won’t pay for damage your home has already sustained. You shouldn’t skimp on liability insurance Many people focus on buying enough coverage for their belongings, but the liability insurance on your policy may be even more important. It pays for injuries or property damage that you’re at fault for. A lawsuit is going to be more devastating than losing your laptop [or] ring. Including legal fees, the cost can total hundreds of thousands of dollars, especially if someone is seriously injured. To protect yourself financially, buy enough liability insurance on your auto and home insurance policies to cover your net worth. Your agent is there to help Confused by your policy’s fine print? Don’t struggle through it on your own. They are there to take care of you and walk you through this process. It's a good idea to interview agents to make sure you trust them and they have the services you need. Once you’ve found an agent you’re comfortable with, it's recommended to touch base once a year or whenever there are changes in your life. This might include getting married, buying a new car or renovating your home, all of which could trigger updates to your insurance. The most important thing to have in your agent is trust, You get so busy with your kids and your job and whatever else you have going on; you shouldn’t have to think about what you need your insurance to do. Source: MSN Money  You can part your hair down the middle and slather on all the wrinkle cream you want — unfortunately, aging is inevitable. Though it may be a tough realization, you are getting older. And that means you should consider getting life insurance, even as a young adult.

Life insurance is designed to provide for your loved ones if (and when) you die. You pay into a policy over time, and after your death your beneficiaries receive a payout to help them make ends meet. It may seem morbid to think about, but it’s a smart way to plan for the future, despite that future still seeming far away. Experts often advise people to look into life insurance when they’re young adults because that can be less complicated and less expensive than purchasing it later. The pandemic has made it even more of a priority: In a recent survey, 19% of Gen Zers and 17% of millennials said they planned to spend more on life insurance this year than last. Members of both age groups identified the pandemic as a major reason for the shift. If you’re among them — or just simply curious — read on to find out how to buy life insurance if you’re young. 1. Figure out whether you need life insurance At its core, life insurance is a contract between a firm and a policyholder who pays regular premiums. If/when the policyholder dies, the firm gives their beneficiaries money to make ends meet. Policies can cover virtually any type of expense, including funeral costs, housing, food and so on. Two other big problems are typically replacement of income to the deceased’s family and elimination of debt in the event of death. Deciding whether to get life insurance is a highly personal decision. It requires asking yourself some tough questions. An easy way to know if you need life insurance is to consider if someone would suffer financially if you were to pass away, if the answer is yes, then you need life insurance. 2. Time it right Purchasing life insurance can feel counterintuitive. The best time to buy life insurance is when you’re young and healthy — even though you (hopefully) won’t need it to kick in until you’re older. The younger you are, the less risky you seem to an insurer, and the lower your premiums are likely to be. The opposite is also true. “If you wait ’til you’re sick or dying, it’s too late, You’ll either be denied a policy or its premiums will be unaffordable. It's recommended to checking in with yourself about it at least once a year. It’s not a bad idea to consider it whenever you tick off a new milestone, as well. Buying a house, getting married, having a kid — those are some of the big life events that cause people to step back and say, ‘Hey, my situation has changed. This might be a time to update my financial plan, and one of those things could be purchasing life insurance. 3. Choose a life insurance type There are two major kinds of life insurance: term and permanent. Term life insurance has a specific time period associated with it. You’ll pay into it for, say, 10 years, and if you’re still alive when the decade is up, your coverage ends. Permanent life insurance can stay in place forever as long as you meet certain criteria. Unlike term life insurance, a permanent policy has an investment value, known as a cash component, that you can tap during your life, to pay premiums or to borrow yourself. That added benefit usually results in higher premiums. (There are subcategories within these types of life insurance, too, including universal and whole.) Consult a financial advisor or independent life insurance company on the best life insurance policy type for you. Working with a financial professional can help you figure out how much coverage you need for your own personal situation. Don’t be shy about calling on one since most are tele-advising, and their expertise can protect you from making financial missteps. 4. Determine the right benefit The policy’s payout, or the so-called “death benefit,” typically ranges from the tens of thousands of dollars to the millions. To figure out what you may need, do some research by determining how much you need in the even your family lost its income. You need to take into consideration what liabilities and assets you have, how much income you’d need to replace, whether you need to plan for education costs, and more to determine how much coverage you need. 5. Find an insurer (and vet them) If you have a job with benefits, you may have some life insurance coverage through work. Though it may help you with your decision, you might want to avoid relying entirely on your work life insurance. It's typically group term life insurance provided for free or at a discount to employees. It’s often not sufficient. Having individual life insurance in addition to your policy through work is important since group life insurance coverage usually ends when you leave your job. When evaluating various insurers, look at how long the company has been around, what its financial strength is, and whether you’ve seen negative headlines about its rates changing. 6. Apply for life insurance Underwriters use risk to determine rates. So to save money on life insurance, experts suggest getting a medical exam to prove how healthy you are. In non-pandemic times, this typically involved blood and urine tests. But the coronavirus crisis changed things. These days, you can simply fill out a questionnaire or give the insurer other personal details, like age, gender, job, driving record and prescriptions. You can get a life insurance policy without even leaving the house. The good news is that these companies are making purchasing life insurance easier than ever, Many companies are using e-signatures, online applications, and sometimes not even requiring blood or urine tests, making life insurance more accessible to more people. 7. Review your policy You’re not done quite yet. After you lock in your life insurance, you need to remember to tweak it as time goes on. Policies often need to be adjusted after a significant life event like getting married, having a baby, getting that promotion at work, starting a business or preparing to retire. Schedule a review with your life insurance agent as soon as possible after a life milestone to make sure you’ve got the right amount of coverage. You might also need to update your life insurance beneficiary. When you’re young and single, you may choose a parent or sibling to receive the payout in case of your death. But you’ll probably want to change that to your spouse or child as you get older. Source: MSN Money  Life insurance comes in many forms, so it’s important to pick the right insurance for you and your family. Although sometimes life insurance can seem like an unnecessary expense, for most families it’s absolutely essential. One of the guiding ideas behind life insurance is to ensure that any large financial obligations are satisfied in the event that your family experiences a loss of income. So, the key to picking the right life insurance for your family is to analyze where your income comes from and what your large financial obligations are. Although every family’s situation is different, here’s a look at some of the most common uses of life insurance and how it can act as a safety net for your family.

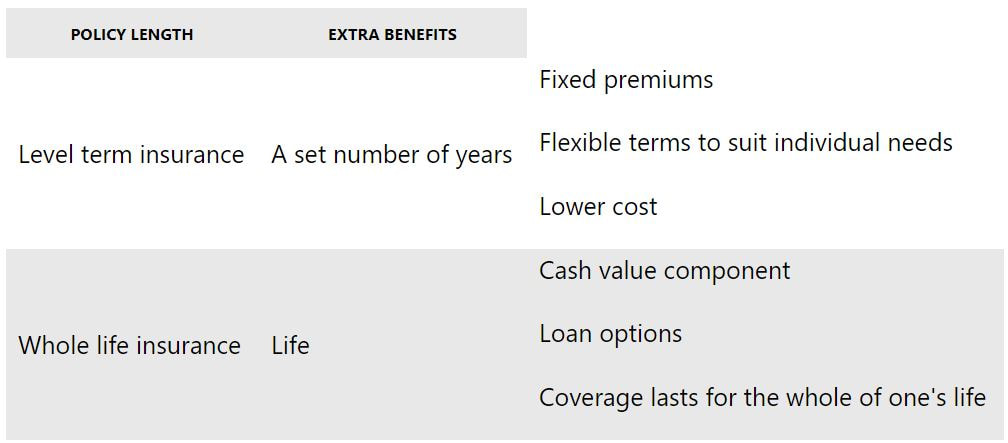

Primary Coverage: Breadwinning Spouse The focus of most life insurance policies is on the breadwinner in the family, for obvious reasons. If a family loses its primary source of income, then the financial security of a family is immediately thrown into doubt. Life insurance can provide a relatively immediate source of funding to take care of a household’s monthly bills until a source of income can be restored. Life insurance comes in many forms, so it’s important to pick the right insurance for you and your family. Although sometimes life insurance can seem like an unnecessary expense, for most families it’s absolutely essential. One of the guiding ideas behind life insurance is to ensure that any large financial obligations are satisfied in the event that your family experiences a loss of income. So, the key to picking the right life insurance for your family is to analyze where your income comes from and what your large financial obligations are. Although every family’s situation is different, here’s a look at some of the most common uses of life insurance and how it can act as a safety net for your family. Secondary Coverage: Nonearning Spouse Although there’s a clear need for insurance coverage for the primary breadwinner in a household, a nonearning spouse should usually be covered as well. Life insurance can help pay for services that used to be covered by the nonearning spouse, such as child care, cleaning or home maintenance. These services, which can often be taken for granted, are quite expensive when you have to hire outsiders. How Much Insurance Do You Need? The specific amount of life insurance you buy will depend greatly on your specific financial circumstances, and you’re best served by discussing your options with a licensed life agent. However, there are some general rules of thumb you can use to approximate how much life insurance you might consider getting. Life insurance in general serves two main purposes: Providing a financial foundation to support your family for years to come and paying off any major debts so that your nonearning survivors don’t have to worry about them. For the financial support portion of the equation, some pundits suggest simply multiplying your annual income by 10 to arrive at a life insurance amount. However, this should be tailored to your family’s specific needs and desires. If you want to provide enough insurance to cover your spouse for the rest of his or her life, along with your kids until they reach the age of majority, simply count up the number of years you want that money to last and multiply that by your annual income. For the debt payoff side of things, first add up all of your debts, including your mortgage, auto loans, college expenses and credit card debt, in addition to any other obligations. Then, subtract your existing liquid assets, including any existing life insurance such as you may have from your employer. If you add up your income replacement needs with the amount you’ll need to pay off all of your debt, you should arrive at a ballpark figure for how much life insurance you might want. How To Find the Best Life Insurance Policy for Your Family There are many kinds of life insurance, from term and whole to universal life insurance and more. The best policy for your family will depend on your needs and a cost/benefit comparison among the different types. Your employer may also offer group rates and varying levels of coverage. To find the best combination, analyze your income, debts and future needs and consulting with at team at USA Mutual Insurance to get started with a Life Insurance policy. Source: MSN Money  What is level term insurance? There are multiple types of term life insurance policies. Rather than covering you for your entire lifespan like whole life or universal life policies, term life insurance only covers you for a designated period of time. Policy terms generally range from 10 years to 30 or more years, although shorter and longer terms may be available. Level term life insurance policies maintain the same death benefit level and premium level over the life of the policy. When applying for a policy, you will specify and list your chosen beneficiaries. You will also select an amount for the death benefit and a length for the policy - for example, you may choose a 10-year term with a $100,000 death benefit. If you pass away during the policy term, your beneficiaries receive the death benefit from the policy. Types of level term insurance Level term life insurance generally comes with one of several policy term options:

Level term versus whole life insurance Whole life is a type of permanent life insurance, meaning that the policy lasts for a person’s lifetime. Term life only lasts for a set length of time, determined when the policy is written. Another key difference is that whole life policies include a cash value investment component while term life does not.  Who needs level term life insurance?

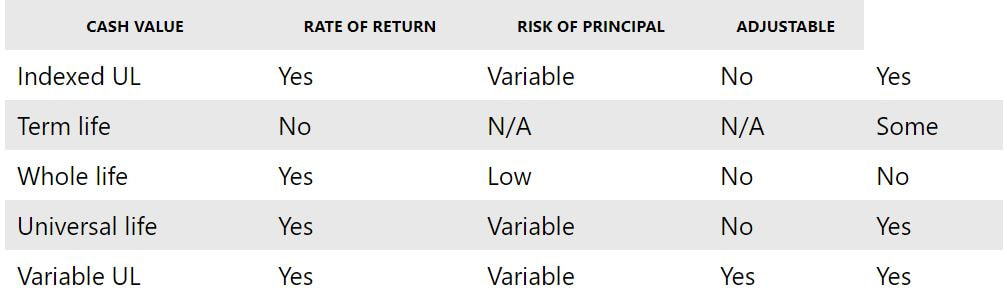

Choosing the right insurance can be tricky. Term life insurance is often recommended over other life insurance types for those who are less experienced with life insurance in general. Part of this may be due to the simplicity and relative cheapness of term life compared to permanent life policies. As a result, people interested in buying life insurance but who are unfamiliar with its nuances might consider starting with term life. Many people choose to purchase level term life insurance when they know they are entering a financially significant time in their lives. People taking out mortgages may decide to buy a term policy that lasts until their mortgage is paid off. People with children going into expensive schools may take out a policy to last until their children are expected to graduate. In general, level term life policies can benefit those entering a period where their loved ones would be disproportionately financially affected by their death. This can span many different scenarios, but the goal of purchasing level term life insurance is to provide compensation for the financial loss associated with the policyholder's passing. What is the cost of level term life insurance? How much is term life insurance? Many factors go into determining the rates on a level term life insurance policy. Two of the most important factors are the term length of the policy and the death benefit amount. Age is another significant component. The older a person is, the more expensive a life insurance policy is likely to be. Health works in a similar way to age. Those who struggle with their health will likely pay higher premiums than those who do not experience health issues. Males are generally more expensive to insure than females. This is partly because women, on average, live longer than men. Risky behaviors may also contribute to policy premiums or may exclude you from coverage. Source: MSN Money  In a nutshell, an indexed universal life insurance policy (IUL) is a form of universal life insurance that pays interest based on the performance of a financial index chosen by your insurer, such as the S&P 500 stock market. The term of this type of policy is divided into crediting periods, also called index periods, which typically range from one month to two years. When the index rises during a given crediting period, the insurance company will credit your policy's cash value with a corresponding amount of interest rather than a fixed interest rate. Indexed universal life insurance policies also normally provide an interest rate guarantee. Those who use the longest crediting periods usually earn the most interest. In most cases, the amount of interest that you can earn during a given crediting period is limited, just like it is with indexed annuities. These limits come in three forms: A "cap" – This is an absolute limit on the amount of interest that is paid. For example, if the benchmark index rises by 30% during a given crediting period, then you may only be able to receive 10% of the growth. The insurance company will keep the difference. A "spread" – This is an amount that the insurance company takes off the top during every crediting period. If the index rises by five percent during a crediting period and your policy has a spread of two percent, then the insurer keeps the first two percent and lets you take the remaining three percent. A "par" rate – This is a participation rate that is a percentage of the growth of the index. If your policy has an 80% par rate, then you will be credited with interest equal to 80% of the growth of the index during that crediting period. Indexed universal life insurance has the same premium and death benefit flexibilities that are found in standard universal life policies. Monthly premiums are adjustable and generally decrease over time as your cash value account increases. Death benefits are also flexible and often have the ability to be lowered or raised at any time. Though your IUL cash value can be accessed freely, it is recommended that this is done with caution as doing so could result in reducing your death benefit or lapsing your account. Who needs indexed universal life insurance? Anyone who is looking for a long-term or permanent life insurance policy, which has the potential to grow cash value at a faster rate than other whole or universal life policies, is a prime candidate for an IUL. Policyholders earn interest at a variable rate and can earn a higher average rate of return over time without risking their money in the stock markets. Indexed universal life insurance vs. other types of life insurance The following table illustrates the similarities and differences between indexed universal life insurance compared with other types of life insurance policies:  Indexed universal life insurance resembles traditional universal life insurance more than any other type of policy. The main difference involves how interest in the cash value is generated. IULs generally have an edge over regular ULs when it comes to overall rate of return, at about 1.5-2% more on average.

Pros and cons of indexed universal life insurance Pros Cash value accumulation Indexed universal life insurance policies have a cash value component which is the part of the policy that is available to you for use while you're still alive. You can use it for anything you want from sending your kids to college to taking a vacation. However, be careful because if you don't pay it all back it can impact the death benefit left to your loved ones. If you don't deplete your cash value by withdrawing from it then this amount (in addition to your death benefit) will be left to your beneficiaries when you die. Tax-free withdrawals The best part about taking money from your cash value? You don't have to pay taxes on it. This is because you've already paid income tax on the money before you've contributed it to your life insurance policy – so you won't have to pay taxes on it again. Adjustable premiums and death benefits Your premiums will adjust over the life of your policy based on the amount of money that's in your cash value component. This allows you to save some money in the long run. Cons Expense Indexed universal life insurance is expensive – in fact, it's one of the most expensive life insurance types out there. It's definitely more expensive than a term policy and so it may be worth considering a more affordable investment option. Variable Interest Rates Your interest rates will vary based on how your money is invested. As the indexes go up, the interest you earn will rise. However, that means that the interest you're earning can go down – or disappear altogether. You're at the mercy of the stock market with this kind of policy. Source: money.msn.com  A life insurance retirement plan (LIRP) can be an effective complement to traditional forms of retirement savings like IRAs or company-sponsored retirement plans. This type of plan does not have many of the distribution-related restrictions that IRAs and qualified plans are saddled with. Although an LIRP is not designed to replace traditional avenues of saving for retirement, it can provide substantial benefits under the right circumstances. Life Insurance Retirement Plans Explained A life insurance retirement plan is a permanent, or cash value life insurance policy that is funded over time, in order to build up a substantial amount of cash value by the time you retire. You can use any type of cash value policy to do this, but some types of coverage have historically grown faster than others - although the policyholder might have had to take on some market risk to get there. LIRPs are designed to provide retirement savers with a supplemental source of income on top of their IRA and retirement plan distributions, after they stop working. LIRPs do not offer some of the tax advantages that IRAs and qualified plans can provide, such as pre-tax or deductible contributions. But they can also provide a few benefits that IRAs and qualified plans cannot match. For example, there is no age requirement for distributions (in the form of tax-free loans) from a LIRP. IRAs and qualified plans will penalize you for any distributions taken before age 59 1/2 , unless a qualified exception applies. Furthermore, LIRPs can often guarantee the investor's principal and interest, unless the investor is contributing to a variable universal life insurance policy. How to Fund Retirement With a LIRP Funding a life insurance retirement plan is very simple. It just requires taking out a cash value life insurance policy for the amount of coverage that you want, then overfunding it by paying more than the minimum required premiums. The excess amount will go into the cash value of the policy and start building it up faster than it would otherwise. This is one of the simplest forms of retirement saving, as there are very few rules that dictate the process. If you want your policy to grow faster over time, consider investing in a variable universal life policy that invests its cash value in the financial markets. There is more risk with this type of policy, but also more reward. Or you could invest in an indexed universal life policy, where you can make money when the financial indices rise but not lose anything when they fall. It all depends on your risk tolerance and time horizon. When you retire, you can take tax-free distributions from your accumulated cash value in the form of policy loans. Of course, it is also possible to take tax-free distributions from your Roth IRA if you have one, but the Roth doesn't also offer death benefit protection and has limits on how much you can put in it each year. Who Needs a Life Insurance Retirement Plan? In the majority of the time, there are three main situations where a LIRP can be appropriate for retirement savers:

Frequently Asked Questions:

What are the best life insurance policies to use for a LIRP? There is no single "best" policy to use for a LIRP; it all depends upon your risk tolerance, time horizon and the amount of money that you're willing to invest. Universal life and indexed universal life policies pay variable rates of interest, but over time they have usually done better than whole life insurance. Risk-takers will want to take a look at variable universal life policies, where there is no limit on their earnings-or losses. How long have LIRPs been around? LIRPs have existed since the first modern commercial cash value life insurance policies were introduced. Anyone who could afford the premiums could set up a LIRP. Higher-income consumers have been using them ever since. But they have become more prevalent with the advent of universal, indexed and variable universal policies that allow the cash value to grow faster than it can inside a traditional whole life policy. How risky are LIRPs compared to IRAs and other retirement plans? It all depends on what type of policy you buy for your LIRP versus what investments you choose in the other alternatives. If you use a whole, universal or indexed universal life policy, then your principal is guaranteed, although the interest rate is variable with the latter two options. If you invest in a variable universal life policy, then you can earn hefty returns when the market goes up. But, of course, the markets don't always do that. The other factor to consider is what you are investing in inside of your IRA or company-sponsored retirement plan. If you are investing primarily in stocks, then you're taking the same amount of risk that you would take with a variable universal policy. If you are investing in government bonds or CDs, then you're taking about as much risk as you are with a whole life policy. You may be contributing to an IRA or qualified plan and have a specific policy in mind to use as a LIRP. If that is the case, it may be wise for you to consult with your financial advisor to compare them. Source: MSN Money  You’ve decorated the tree, put up the lights and placed a lit candle in every window. But the next thing you know, you smell smoke.

Candle fires, stolen presents and other calamities can put an unwelcome damper on your seasonal cheer, but insurance can often help clean up the mess. Here are some common holiday disasters and how your homeowners insurance can come to the rescue. 1. Decorations catch fire “Chestnuts roasting on an open fire” takes on a whole new meaning when the halls are decked with fire hazards. Dehydrated Christmas trees can go up in flames if placed too close to a heat source, and fires from candles make up half of December home decoration fires, according to the U.S. Fire Administration. Fire is covered in three main ways. Dwelling coverage pays for repairs to your home, while other structures coverage is for things like a detached garage or fence. Personal property coverage will pay to replace damaged belongings, up to your policy limits. To avoid festive fires, keep candles away from flammable objects, follow all manufacturer instructions for holiday lights outside and keep a real Christmas tree hydrated. 2. Your identity gets stolen If you’ve shopped online for holiday gifts this year, your credit card or bank account information may be at risk of getting stolen. Identity theft coverage can pay for out-of-pocket expenses related to identity theft or fraud. Some homeowners insurance policies automatically include this coverage for free, but you’ll probably have to add it to your policy. You can reduce the risk of identity theft from online shopping by avoiding unsecured networks and by purchasing from trusted stores — check for a privacy policy on the site and a padlock to the left of the URL. To protect yourself from potential data breaches, reenter account information with every purchase instead of allowing online vendors to store your information. 3. Presents get stolen If expensive holiday gifts go missing, don’t pout. Your personal property coverage covers items stolen from your home and car, up to your policy limits. To prevent any grinches from stealing holiday presents, avoid letting packages sit unattended and consider setting up a security camera system around your home. If you leave gifts in the car, tuck them away safely in the trunk, lock the doors and park in a well-lit location. If gifts are stolen, file a claim with your insurance company only if their value exceeds your deductible. 4. A guest gets injured Say you undercook the turkey and send relatives to the hospital. Maybe someone breaks a hip on your icy walkway, or the dog bites a guest. You could end up on the hook for their medical costs. The medical expense coverage in your home insurance policy pays to treat your sick or injured guests, no matter who's legally responsible, while your personal liability coverage will cover you in case they decide to sue. Because of the pandemic, you may be skipping holiday gatherings entirely this year. But if you do host guests, make sure you abide by the guidelines for small gatherings from the Centers for Disease Control and Prevention, or CDC, which include wearing face masks and practicing social distancing. 5. A water pipe bursts If a pipe gets cold enough, water freezes and expands inside, increasing the chance of a burst. Water damage from burst pipes is generally covered by home insurance, but check the fine print in your policy, as you’re covered only if the burst is accidental and not due to poor maintenance. To avoid damage, watch for warning signs of frozen pipes, such as low water pressure or frost on the outside of the pipe. To offset the chance of a water burst:

Source. money.msn.com  Perhaps fueled by acute awareness of their own mortality, many Americans shopped for life insurance during the pandemic. But some lost interest when local Covid-19 cases declined.

More than a third of those who considered purchasing life insurance due to the pandemic — but ultimately didn't buy — say they decided against it because Covid-19 cases in their area started going down. This behavior suggests some people view life insurance as a "panic purchase". If the pandemic highlighted a hole in your coverage, you'll likely need to address it regardless of how Covid-19 cases evolve. Learn how to determine whether you need life insurance, despite current events, and get the right coverage for you and your loved ones. Why Some Shoppers Decided Against Life Insurance Conducted online by The Harris Poll, NerdWallet's survey asked U.S. adults who considered buying life insurance due to the pandemic, but ultimately chose not to, why they decided against it. 35% say their decision not to buy coverage was because Covid-19 cases in their area started going down. 25% say it was too expensive. 24% decided their workplace coverage was sufficient. Whether you need life insurance, how much you should buy and how much you should spend are not easy questions to answer. In the survey, 17% of Americans who considered buying life insurance due to the pandemic but decided against it say it's because they don't understand how it works, and 14% say they didn't know where to start. Unraveling these concerns can help you set up a more robust life insurance plan. How to Determine if You Need Life Insurance Immediate threats like the pandemic may highlight a need, but they shouldn't dictate your buying decision. After all, an unexpected death could come at any time, not just due to Covid-19. Similarly, just because you're suddenly conscious of what you'd be leaving behind, it doesn't automatically mean you need life insurance. Before you shop for coverage, ask yourself these questions: Will Your Death Create a Financial Burden? You typically need life insurance if your death would place a financial burden on others. The type of burden is different for everyone. For example, you may need a large policy to support a spouse or children for several years, or a smaller one to cover final expenses, like burial costs. A quick way to estimate the amount of coverage you need is to add up your long-term financial obligations and subtract your assets. Another popular rule is to multiply your income by 10. But these quick tricks are just a guide. Online calculators can help you determine how much life insurance you need. Is the Financial Burden Temporary? How long other people will rely on you financially can dictate the type of life insurance you need. For example, if you're supporting a child through college, consider a term life policy that covers only the years you need. Term life lasts a set number of years and is typically less expensive than permanent life insurance. Alternatively, if you plan to support a family member for the foreseeable future, you might want to consider a permanent life insurance policy, as coverage lasts your entire life. Is Your Workplace Life Insurance Enough? After calculating the amount of life insurance you need, check whether you already have sufficient coverage. In March 2020, nearly 6 in 10 American civilian workers participated in a workplace life insurance plan. However, group life insurance provided by an employer is generally one to two times your annual salary, which may fall short of what you need. And life insurance through work is typically tied to your employment, meaning if you lose your job, you may lose your coverage. Ultimately, life insurance is purchased for a need, someone can catch coronavirus and pass away, but someone can just as easily get in their car tomorrow and die in a car accident. So, if the need is there, the need is there. Source: money.msn.com and nerdwallet.com |

Archives

February 2022

Categories |

RSS Feed

RSS Feed